Navigating Insurance Uncertainty: A Must-Read for San Mateo County Homeowners

Greene & Sievers Real Estate Team • February 3, 2025

NAR Changes

PENINSULA INSIGHTS | JANUARY EDITION

Helping homeowners on the peninsula navigate life and home transitions with ease.

PENINSULA INSIGHTS | SPRING 2025 EDITION Helping homeowners on the peninsula navigate life and home transitions with ease.

PENINSULA INSIGHTS | FEBRUARY EDITION Helping homeowners on the peninsula navigate life and home transitions with ease.

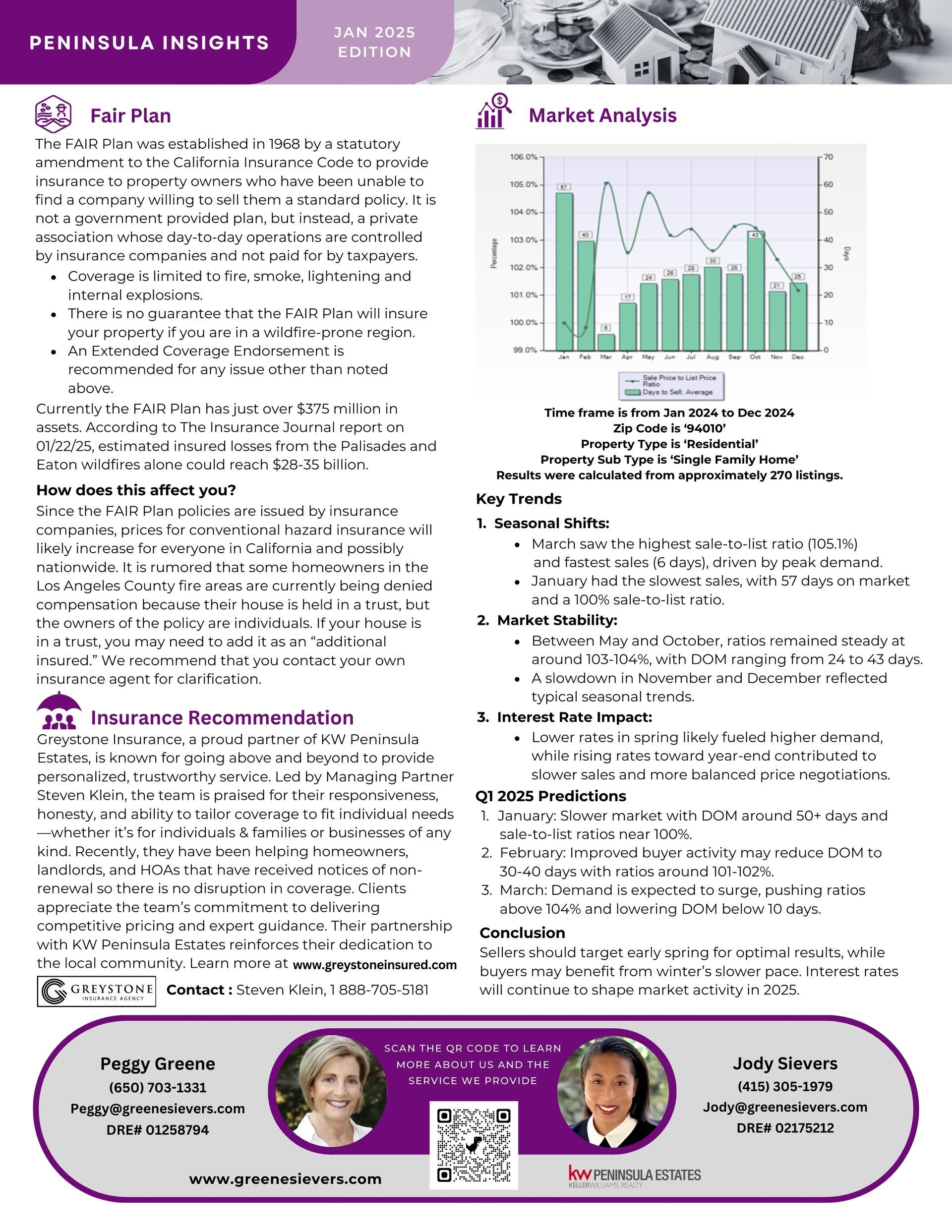

PENINSULA INSIGHTS | WINTER EDITION Helping homeowners on the peninsula navigate life and home transitions with ease.

PENINSULA INSIGHTS | OCTOBER EDITION Helping homeowners on the peninsula navigate life and home transitions with ease.

PENINSULA INSIGHTS | SEPTEMBER EDITION Helping homeowners on the peninsula navigate life and home transitions with ease.

PENINSULA INSIGHTS | JULY EDITION Helping homewoners on the peninsula navigate life and home transitions with ease.

Congratulations! Top Performer!

This June, we provide a comprehensive market update and shine a spotlight on our trusted vendors, all while helping homeowners on the Peninsula navigate home transitions with ease.

A balcony adds so much to a living space. Especially in an apartment if you don't have a yard, it can serve as a place for coffee in the morning, a place to read a book on a sunny afternoon, or even a place to set out a few herb plants. But safety is paramount, especially when it comes to balconies and decks. Two new key pieces of legislation, SB 721 and SB 326, address this concern by mandating inspections of Exterior Elevated Elements (EEEs) in multi-family buildings. Here's a breakdown of both bills and their key differences: Similarities: Focus: Both SB 721 and SB 326 aim to ensure the safety of residents by requiring regular inspections of EEEs like balconies, decks, walkways, and stairways. Inspection Requirements: Both bills require inspections to be conducted by qualified professionals like architects, structural engineers, or licensed general contractors. The inspections will assess waterproofing, structural integrity, and overall safety. Timeline: The initial inspection deadline is January 1, 2025, for all covered buildings. Subsequent inspections will occur at regular intervals – every six years for SB 721 and every nine years for SB 326. Differences: Who They Affect: SB 721 applies to landlords of buildings with three or more multi-family dwelling units that are at least two stories tall. Think apartment buildings. SB 326 focuses on condominium and townhouse associations for similar multi-unit buildings. Frequency of Inspections: SB 721 requires more frequent inspections, happening every six years compared to SB 326's nine-year interval. Estimated Inspection Cost: The cost of an inspection can vary depending on factors like the size and complexity of the building, the number of EEEs, and the inspector's qualifications. However, estimates typically range from $300 to $500 per balcony, with additional fees for inspecting other EEEs. It's important to note that for homes with HOAs, the management company, not you, is responsible for organizing the inspections and associated repairs. Overall, both SB 721 and SB 326 are crucial steps towards ensuring the safety of Californians living in multi-family buildings with balconies and other EEEs. Understanding which bill applies to your specific situation (landlord vs. homeowner association) is essential for complying with the inspection deadlines. For more details and resources: California Department of Housing and Community Development (HCD): https://www.hcd.ca.gov/ (Look for information on SB 721 and SB 326) California Architects Board (CAB): https://www.cab.ca.gov/ (Provides a directory of licensed architects who may conduct inspections) California Structural Engineers Association (CSEA): https://seaosc.org/ (Provides a directory of licensed structural engineers who may conduct inspections)

Did you know that you can use 1031 exchange funds for renovation expenses? I was recently chatting with a client who owns an investment property and was considering a 1031 Exchange – swapping a new property that's "like-kind" for an existing one, while deferring capital gains taxes. I shared something they were not familiar with, which was they could actually use a portion of those exchange funds for renovations on the new property. It is specifically referred to as an improvement exchange. By doing this they could potentially: Defer capital gains taxes on the sale of their existing property, by reinvesting the proceeds into the replacement property and improvements, allowing their money to grow tax-deferred. Increase the new property’s value by using sale proceeds for improvements on the replacement property. This can also result in higher rental income or a larger profit when you eventually sell. Customize the replacement property to perfectly suit your investment goals. It's important to remember that this is a complex tax strategy. There are strict time constraints, the replacement property must be "like-kind," and working with both a 1031 Qualified Intermediary (A neutral third-party middleman, facilitating the exchange process and ensuring compliance with IRS regulations) and a tax advisor is crucial for a smooth and compliant tax-deferred exchange. If you would like to learn more about this strategy, contact us via e-mail at Team@greenesievers.com to schedule a time to meet. We can also put you in touch with a 1031 specialist who can further explain the details of this approach.